The 7-Second Trick For Kam Financial & Realty, Inc.

The 7-Second Trick For Kam Financial & Realty, Inc.

Blog Article

More About Kam Financial & Realty, Inc.

Table of ContentsThe Facts About Kam Financial & Realty, Inc. RevealedThe smart Trick of Kam Financial & Realty, Inc. That Nobody is DiscussingKam Financial & Realty, Inc. Can Be Fun For Everyone8 Simple Techniques For Kam Financial & Realty, Inc.A Biased View of Kam Financial & Realty, Inc.3 Simple Techniques For Kam Financial & Realty, Inc.Some Known Questions About Kam Financial & Realty, Inc..

The home acquiring procedure entails numerous steps and variables, suggesting each individual's experience will certainly be one-of-a-kind to their household, financial situation, and wanted building. That does not mean we can't aid make feeling of the home loan process.A is a kind of finance you use to get building, such as a home. Normally, a loan provider will certainly offer you a collection amount of cash based on the worth of the home you want to buy or possess.

Some Of Kam Financial & Realty, Inc.

To certify for a home mortgage finance, you will certainly require to be at the very least 18 years old. Variables that assist in the mortgage process are a trusted revenue resource, a strong credit report, and a moderate debt-to-income ratio. (https://urlscan.io/result/955ff859-6761-409a-8342-610d6278222a/). You'll find out more regarding these consider Module 2: A is when the homeowner obtains a new home mortgage finance to change the one they currently have in area

A features similarly to an initial mortgage. You can obtain a set quantity of money based on your home's equity, and pay it off through dealt with monthly payments over a set term. An operates a bit in different ways from a conventional home mortgage financing and resembles a charge card. With a HELOC, you receive approval for a taken care of quantity of cash and have the adaptability to obtain what you need as you need it.

This co-signer will certainly agree to pay on the mortgage if the customer does not pay as concurred. Title business play a vital role ensuring the smooth transfer of residential property possession. They investigate state and area records to verify the "title", or possession of your home being bought, is cost-free and free from any kind of various other mortgages or commitments.

All About Kam Financial & Realty, Inc.

Additionally, they offer written guarantee to the loan provider and create all the documentation needed for the mortgage. A deposit is the amount of cash money you should pay ahead of time towards the acquisition of your home. If you are acquiring a home for $100,000 the lending institution may ask you for a down settlement of 5%, which implies you would certainly be required to have $5,000 in money as the down repayment to acquire the home. (https://www.awwwards.com/kamfnnclr1ty/).

A lot of lending institutions have traditional home mortgage standards that enable you to obtain a certain percentage of the value of the home. The percentage of principal you can borrow will vary based on the home loan program you qualify for.

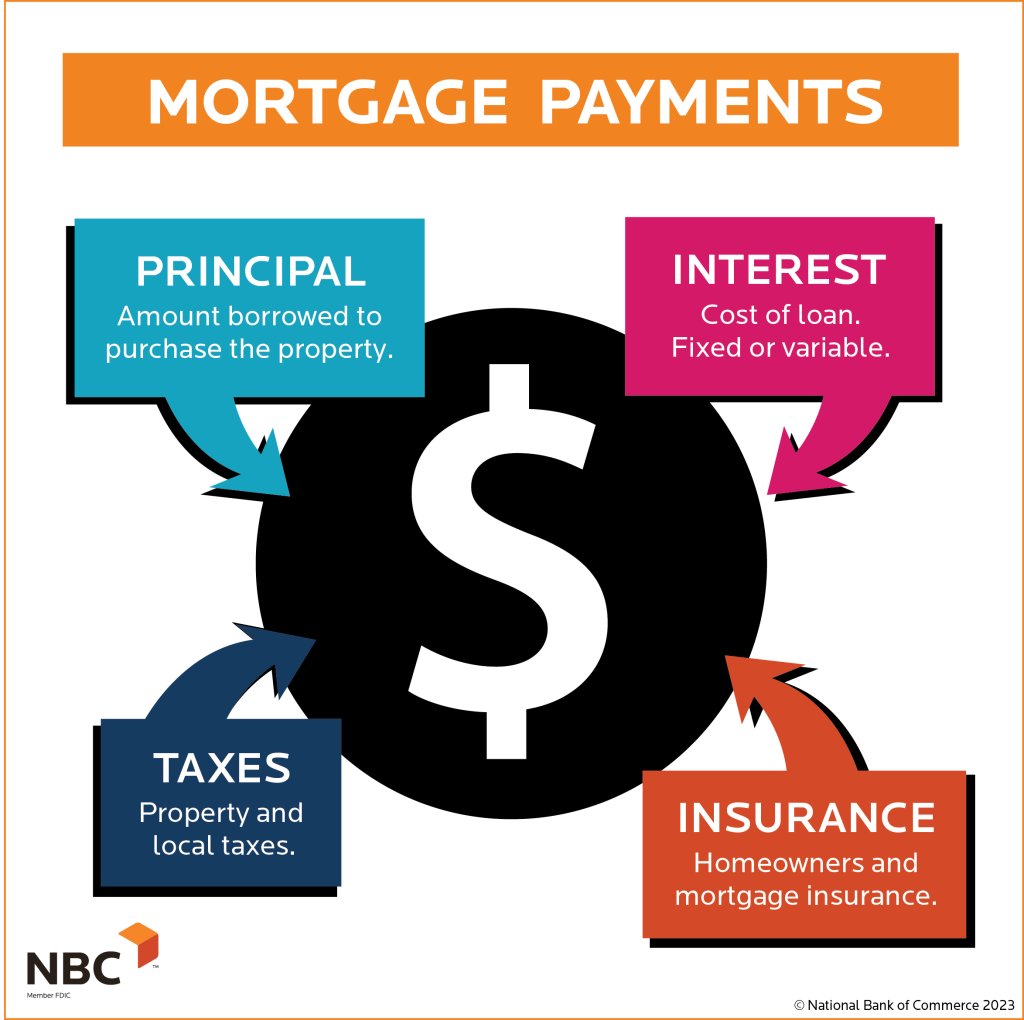

There are special programs for novice home customers, veterans, and low-income customers that allow reduced deposits and greater percents of principal. A home mortgage banker can evaluate these choices with you to see if you certify at the time of application. Passion is what the loan provider fees you to borrow the cash to acquire the home.

Some Of Kam Financial & Realty, Inc.

If you were to secure a 30-year (360 months) mortgage and borrow that exact same $95,000 from the above example, the total amount of passion you would pay, if you made all 360 monthly payments, would be a little over $32,000. Your month-to-month repayment for this car loan would be $632.

A lot of lending institutions will certainly require you to pay your tax obligations with your mortgage payment. Residential property tax obligations on a $100,000 funding can be about $1,000 a year.

Getting The Kam Financial & Realty, Inc. To Work

Once again, since the home is viewed as collateral by the lending institution, they intend to see to it it's shielded. Property owners will certainly be needed to provide a copy of the insurance plan to the loan provider. The annual insurance plan for a $100,000 home will certainly cost roughly $1,200 a year. Like taxes, the lending institution will certainly additionally offeror sometimes requireyou to include your insurance premium in your regular monthly payment.

Your settlement now would boost by $100 to a brand-new overall of $815.33$600 in principle, $32 in rate of interest, $83.33 in tax obligations, and $100 in insurance coverage. The loan provider holds this money in the exact same escrow account as your residential or commercial property taxes and makes payments to the insurance policy company in your place. Closing expenses describe the expenses related to refining your car loan.

4 Easy Facts About Kam Financial & Realty, Inc. Explained

This ensures you comprehend the overall expense and accept continue prior to the lending is moneyed. There are many different programs and loan providers you can select from when you're getting a home and obtaining a home mortgage that can aid you browse what programs or choices will certainly function best for you.

Kam Financial & Realty, Inc. Things To Know Before You Get This

Many economic establishments and property agents can help learn the facts here now you recognize just how much money you can spend on a home and what funding quantity you will get approved for. Do some research, yet likewise ask for referrals from your close friends and family members. Discovering the right companions that are a great fit for you can make all the distinction.

Report this page